Jay Roth, Elsner Engineering Works09.01.21

Anyone involved in the wipes industry knows the roller coaster of a ride we are on. When viewed through a narrow window, it looks like we are an unstable lot with extreme peaks and valleys. However, when viewed over a greater period of time we see that we are a healthy, steadily growing marketspace.

Looking specifically at the canister wipes market, we’ve seen remarkable growth and demand over the past few decades. Canister wipes entered the market in force in the 1980s with baby wipes and some mild claim hand wipes as the first products on the shelves. The first production machines were re-purposed from other applications. For Elsner, this was the V-Series rewinder with our rotary shear-type perforator originally put into use converting fabric softener into a sheets-on-a-roll format. Production started at narrow widths, making one roll at a time. Adapting this to the nonwovens used in wipes, many used a 30-inch wide web. The machine would perforate and rewind a full 30-inch log, then transfer it to a log saw with fixed position blades to cut the ‘log’ into finished roll sizes (typically around 6 inch cuts).

As demand increased converters needed to better match up converting equipment capacity with the deckle width of the nonwovens suppliers. For many, a 42-inch machine met that need and this is where we focused our automated machinery for rolled wipes converting.

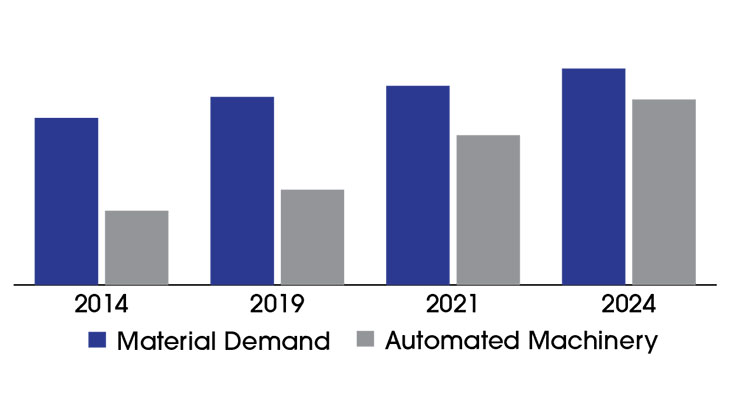

The canister wipes market has really taken off in the past 15 years or so. Figure 1 shows a comparison of the amount of nonwoven used in wipes applications (using data from the INDA’s North American Nonwovens Industry Outlook 2019-2024) we show a comparison of material demand increase versus known (ELSNER and others) automated wipes machinery output. There is variability in the numbers due to the wide range of wipe sizes, OEE (Overall Equipment Efficiency), sheet counts, etc…the general trend towards automation was the major gamechanger in this market. The gap is narrowing as older equipment and methods are retired and new, faster machines are put into place. Of course, there was a significant spike in 2020 and 2021 due to Covid inflated demand, but, again, the overall industry outlook remains the same. For brand owners, the numbers will likely settle out at or perhaps a few ticks higher than 2019 projections. For machine builders, the impact will last longer. This type of equipment is not made to use for a quick fill, this added capacity is going to remain in place for a long time.

One of the more entertaining parts of my job is keeping confidential information in an industry where everybody knows everybody. I get needled by customers asking who else I am visiting in the area when I travel to see them. Then they tell me that they already know; that their friend or neighbor works for their competitor, or their maintenance tech has just come over from the company down the road. I see quick exchanges at events and trade shows where owners, sales teams and others are seated next to each other, rubbing elbows at the evening reception or taking a few steps away from the crowds for a chat. My first robotics team calls that ‘gracious professionalism.’ There is no need for ill will as we all vie for a piece of the pie.

With that, very few customers like to promote what equipment they use, how many or how new. So I’ve had to scrub the data a little here, but will provide a snapshot of a few of the different customer models that operate in the canister wipes industry.

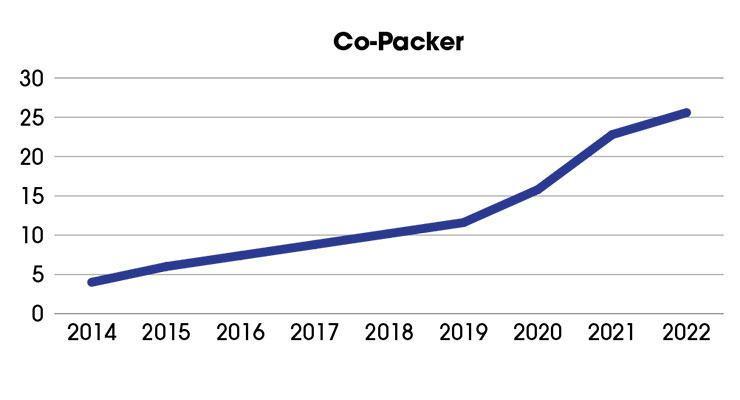

First is a ‘Co-Packer’…a company focused on providing efficient converting operations for one or many brand owners. You can see competitive products running side by side, or even one after the other on the same machine. The benefit is that they are not reliant on a single source or brand dominance. If one slips, the other will make up for it…hopefully. They can focus on their operations and being the best partner to the brand owners.

This ‘Case Study’ shows one such Co-Packer. Steady growth from 2014 thru 2022 in regards to canister wipes production capacity. Pretty smooth growth, with the noted Covid bump from 2020 to 2021.

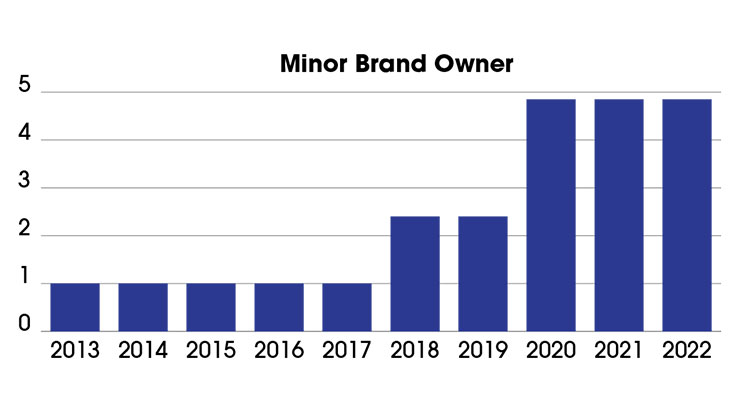

Case Study #2 shows a ‘minor’ Brand Owner. What we often see is a brand starts by using a co-packer and keeps an eye on numbers as they go, bringing converting in-house when production numbers are well established. Choppier growth. Sort of an ‘all eggs in one basket’ situation. Their brand has to perform, more incremental growth than a bigger player, but overall eventually the same upward trend.

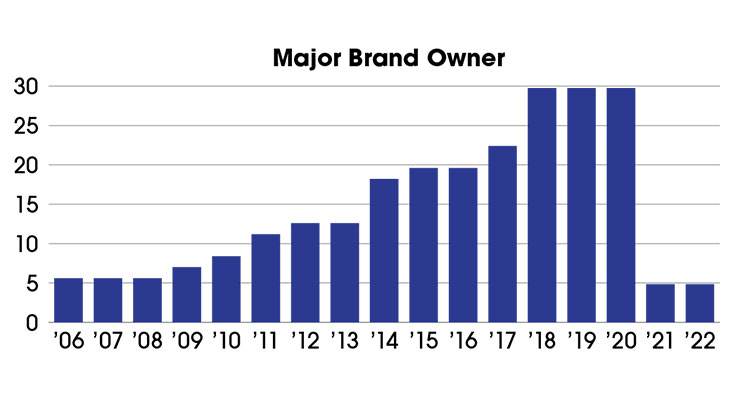

Case Study #3 shows a ‘Major’ Brand Owner. This one had a big jump from 2017 to 2018, but the overall trend is much the same. They control their own destiny. They can ramp up when they need, sometimes these guys will flex capacity to a co-packer if there is a sudden increase in demand, or a big swing in marketshare. Still a little choppier than the co-packer model, where they spread their bet over a number of horses instead of just betting on the winner.

We found a need in the market for a low volume co-packer/R&D model. New entrants into wipes had great ideas, but with limited initial volumes they were unattractive to established co-packers. Businesses such as the Elsner Tech Center added the capability…great flexibility, but higher costs and limitations on long term growth. Pre-Covid we thought this volume was anything under 20,000 canisters and/or with no guarantee of a long term contract. We saw this happen once when a new company came to Elsner. We first provided a list of co-packer customers but there was ‘no room at the Inn.’ We helped with the first production run and the client had market acceptance and came back for round two. Again, they saw success and sold out of their second stock of inventory quickly. Coming back for round three, they now had something that would be attractive to an established co-packer and they were starting to look at efficiencies that would be better served outside of an R&D setup. Round three was completed by a co-packer and quickly moved to Round four….enter Covid. Confident with an order for 50,000 units the wipes team sent in their repeat order, but, the co-packer no longer had room. Re-enter the Tech Center model. If there is a benefit to Covid, it was in the growth of our industry. As we exit Covid, we may see this settle back to a lower number but for now the bar has been raised. Co-packers and brand owners alike have seen demand skyrocket. We are starting to see some settling and less panic, but where will we land? I think those who had their ducks in a row prior to Covid and were poised for growth are coming out shining. Those who went ‘all in’ on new ventures and short term opportunity may have a bumpy road ahead.

Everyone would like a roadmap to show us where canister wipe demand will go in the next decade. Sharing information and insight through publications like this, meetings with others in the industry individually and participating in events like INDA’s recent World of Wipes Conference, we can help each other navigate this exciting market. I think the following provides a summary of where canister wipes machinery demand stands currently. Although Covid has resulted in a spike in demand and new equipment being put into production, I do not think we have reached over-saturation. We are seeing a short term leveling, but longer term growth will stay on track (meaning we may have added two or three years worth of capacity growth in a single year, but five year plans remain the same). Automation will continue to rise. Covid has shown us the need to adapt to rapid changes in available workforce. Less reliance on people creates a more stable production environment. There will still be plenty of work for our production teams, automation makes life easier and allows people to use their talents for more fulfilling tasks.

Looking specifically at the canister wipes market, we’ve seen remarkable growth and demand over the past few decades. Canister wipes entered the market in force in the 1980s with baby wipes and some mild claim hand wipes as the first products on the shelves. The first production machines were re-purposed from other applications. For Elsner, this was the V-Series rewinder with our rotary shear-type perforator originally put into use converting fabric softener into a sheets-on-a-roll format. Production started at narrow widths, making one roll at a time. Adapting this to the nonwovens used in wipes, many used a 30-inch wide web. The machine would perforate and rewind a full 30-inch log, then transfer it to a log saw with fixed position blades to cut the ‘log’ into finished roll sizes (typically around 6 inch cuts).

As demand increased converters needed to better match up converting equipment capacity with the deckle width of the nonwovens suppliers. For many, a 42-inch machine met that need and this is where we focused our automated machinery for rolled wipes converting.

The canister wipes market has really taken off in the past 15 years or so. Figure 1 shows a comparison of the amount of nonwoven used in wipes applications (using data from the INDA’s North American Nonwovens Industry Outlook 2019-2024) we show a comparison of material demand increase versus known (ELSNER and others) automated wipes machinery output. There is variability in the numbers due to the wide range of wipe sizes, OEE (Overall Equipment Efficiency), sheet counts, etc…the general trend towards automation was the major gamechanger in this market. The gap is narrowing as older equipment and methods are retired and new, faster machines are put into place. Of course, there was a significant spike in 2020 and 2021 due to Covid inflated demand, but, again, the overall industry outlook remains the same. For brand owners, the numbers will likely settle out at or perhaps a few ticks higher than 2019 projections. For machine builders, the impact will last longer. This type of equipment is not made to use for a quick fill, this added capacity is going to remain in place for a long time.

One of the more entertaining parts of my job is keeping confidential information in an industry where everybody knows everybody. I get needled by customers asking who else I am visiting in the area when I travel to see them. Then they tell me that they already know; that their friend or neighbor works for their competitor, or their maintenance tech has just come over from the company down the road. I see quick exchanges at events and trade shows where owners, sales teams and others are seated next to each other, rubbing elbows at the evening reception or taking a few steps away from the crowds for a chat. My first robotics team calls that ‘gracious professionalism.’ There is no need for ill will as we all vie for a piece of the pie.

With that, very few customers like to promote what equipment they use, how many or how new. So I’ve had to scrub the data a little here, but will provide a snapshot of a few of the different customer models that operate in the canister wipes industry.

First is a ‘Co-Packer’…a company focused on providing efficient converting operations for one or many brand owners. You can see competitive products running side by side, or even one after the other on the same machine. The benefit is that they are not reliant on a single source or brand dominance. If one slips, the other will make up for it…hopefully. They can focus on their operations and being the best partner to the brand owners.

This ‘Case Study’ shows one such Co-Packer. Steady growth from 2014 thru 2022 in regards to canister wipes production capacity. Pretty smooth growth, with the noted Covid bump from 2020 to 2021.

Case Study #2 shows a ‘minor’ Brand Owner. What we often see is a brand starts by using a co-packer and keeps an eye on numbers as they go, bringing converting in-house when production numbers are well established. Choppier growth. Sort of an ‘all eggs in one basket’ situation. Their brand has to perform, more incremental growth than a bigger player, but overall eventually the same upward trend.

Case Study #3 shows a ‘Major’ Brand Owner. This one had a big jump from 2017 to 2018, but the overall trend is much the same. They control their own destiny. They can ramp up when they need, sometimes these guys will flex capacity to a co-packer if there is a sudden increase in demand, or a big swing in marketshare. Still a little choppier than the co-packer model, where they spread their bet over a number of horses instead of just betting on the winner.

We found a need in the market for a low volume co-packer/R&D model. New entrants into wipes had great ideas, but with limited initial volumes they were unattractive to established co-packers. Businesses such as the Elsner Tech Center added the capability…great flexibility, but higher costs and limitations on long term growth. Pre-Covid we thought this volume was anything under 20,000 canisters and/or with no guarantee of a long term contract. We saw this happen once when a new company came to Elsner. We first provided a list of co-packer customers but there was ‘no room at the Inn.’ We helped with the first production run and the client had market acceptance and came back for round two. Again, they saw success and sold out of their second stock of inventory quickly. Coming back for round three, they now had something that would be attractive to an established co-packer and they were starting to look at efficiencies that would be better served outside of an R&D setup. Round three was completed by a co-packer and quickly moved to Round four….enter Covid. Confident with an order for 50,000 units the wipes team sent in their repeat order, but, the co-packer no longer had room. Re-enter the Tech Center model. If there is a benefit to Covid, it was in the growth of our industry. As we exit Covid, we may see this settle back to a lower number but for now the bar has been raised. Co-packers and brand owners alike have seen demand skyrocket. We are starting to see some settling and less panic, but where will we land? I think those who had their ducks in a row prior to Covid and were poised for growth are coming out shining. Those who went ‘all in’ on new ventures and short term opportunity may have a bumpy road ahead.

Everyone would like a roadmap to show us where canister wipe demand will go in the next decade. Sharing information and insight through publications like this, meetings with others in the industry individually and participating in events like INDA’s recent World of Wipes Conference, we can help each other navigate this exciting market. I think the following provides a summary of where canister wipes machinery demand stands currently. Although Covid has resulted in a spike in demand and new equipment being put into production, I do not think we have reached over-saturation. We are seeing a short term leveling, but longer term growth will stay on track (meaning we may have added two or three years worth of capacity growth in a single year, but five year plans remain the same). Automation will continue to rise. Covid has shown us the need to adapt to rapid changes in available workforce. Less reliance on people creates a more stable production environment. There will still be plenty of work for our production teams, automation makes life easier and allows people to use their talents for more fulfilling tasks.